By Peter Theisen

A world of decreased friction; advocates of open banking say that the rise of open data will unchain the finance function through more transparency, flexibility, innovation, and choice.

With open finance gathering momentum, it has the potential to significantly alter the global operations of the financial services ecosystem. It could challenge conventional banking models, causing a shift in the way we understand finance, and putting pressure on established players. Practically, how does this matter for the finance leader?

We will highlight five core ways:

- Streamlined Automation in Financial Operations,

- Improved forecasting and cash flow in Business Finance Management,

- Getting Closer to Customers and their Financial Operations,

- Data Analytics-Driven Financial Management Tools to Aid and

- Decreased human friction — let my people self-serve.

But first, let's quickly get on the same page: What is open finance?

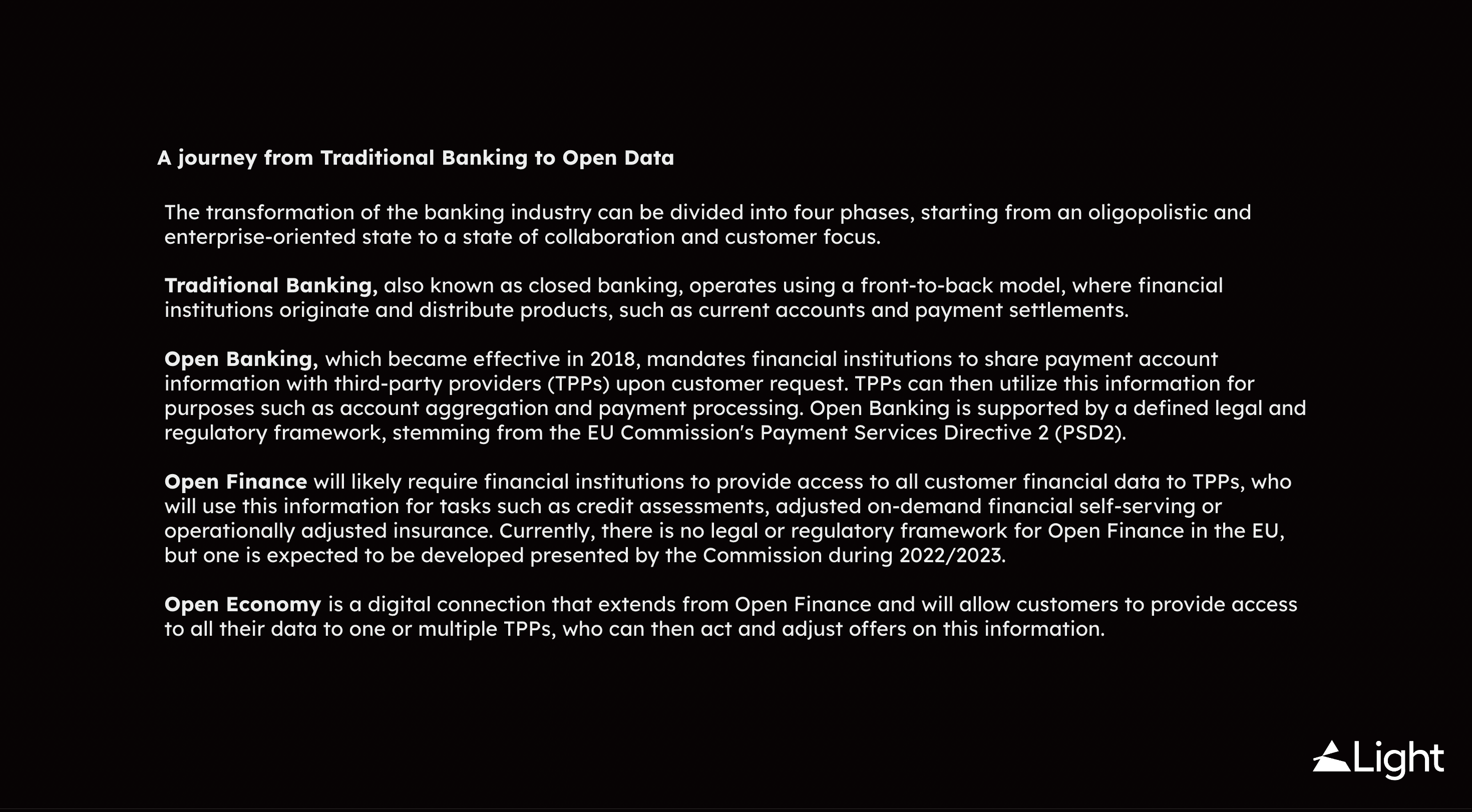

The Journey from Traditional Finance to an Open Data Economy

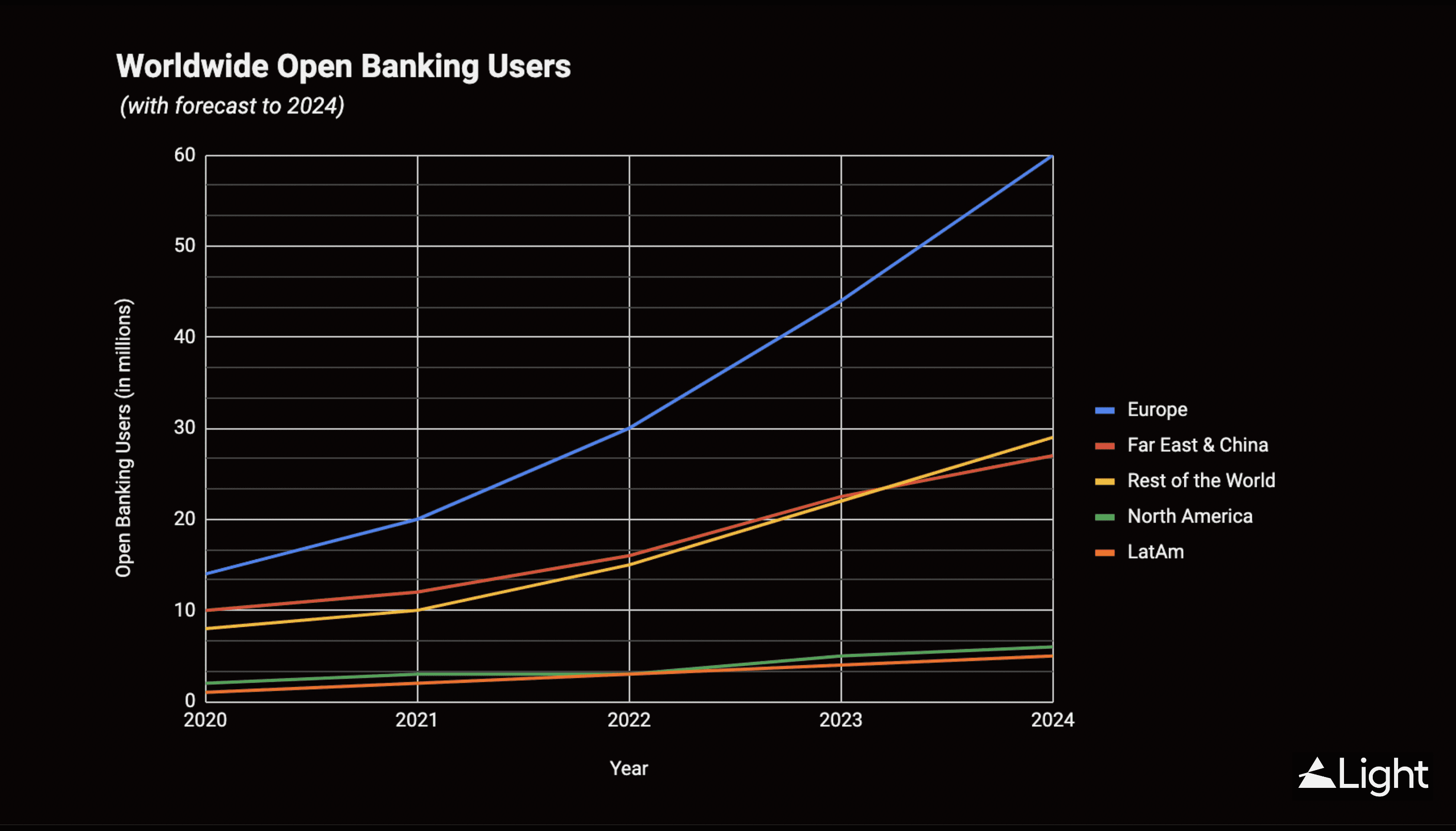

In a nutshell, open banking refers to a system where customers give third-party providers (TPPs) permission to access their financial data held by banks. The objective of open banking is to increase competition in the financial services industry, provide greater financial choice and improve the customer experience. The global open banking market is expected to grow at a compounded annual rate of 50% from 2020 to 2024 - with Europe being a key market.

The adoption of open banking is rapidly increasing and is poised to have a significant impact on the finance leader. Europe and the UK have been among the early adopters, and this trend is expected to persist with the progression of open finance. In the U.K. alone, open banking use has exploded in popularity, going from around 15 million API calls per day in July 2020 to nearly 33 million just two years later.

Figure 1: Worldwide Open Banking Users. Source: Statista, 2022, graphic created by Light.

Open Banking has sparked a revolution by empowering end-users as the owners of their financial data. The finance department now has the ability to freely share it with any party of their choice, whether it be a financial institution or not.

Open Finance, on the other hand, refers to a broader systemic concept that indeed encompasses the idea of open banking — and then goes beyond just banking. The concept was introduced in the European Commission's Digital Finance Strategy released in 2020 and has since generated significant interest and discussion in the financial sector. However, what do we currently know about Open Finance?

It refers to a movement in the financial industry towards greater financial openness, innovation, and accessibility. It encompasses a range of financial services, including traditional banking services, alternative financial services, and new forms of finance made possible by digital technology.

So with its reach extending beyond just payments that Open Banking deals with, Open Finance is poised to impact a wide range of areas in finance, like Ledgers, Banks and FIs, AP and AR workflows, Risk and Analytics, Workflow Automation. In essence, Open Finance has the potential to touch all aspects of a customer's financial profile.

Figure 2: From Traditional Banking to an Open Data Economy, created by Light

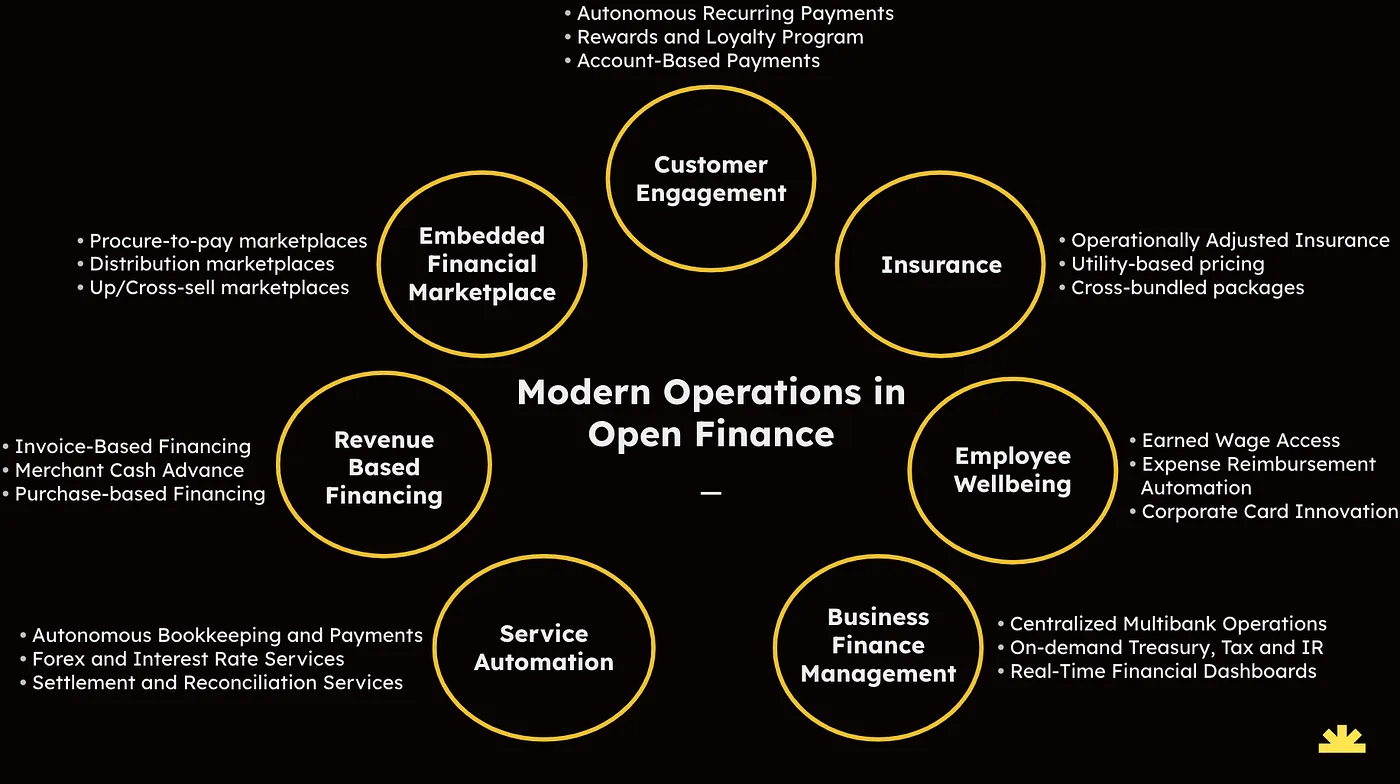

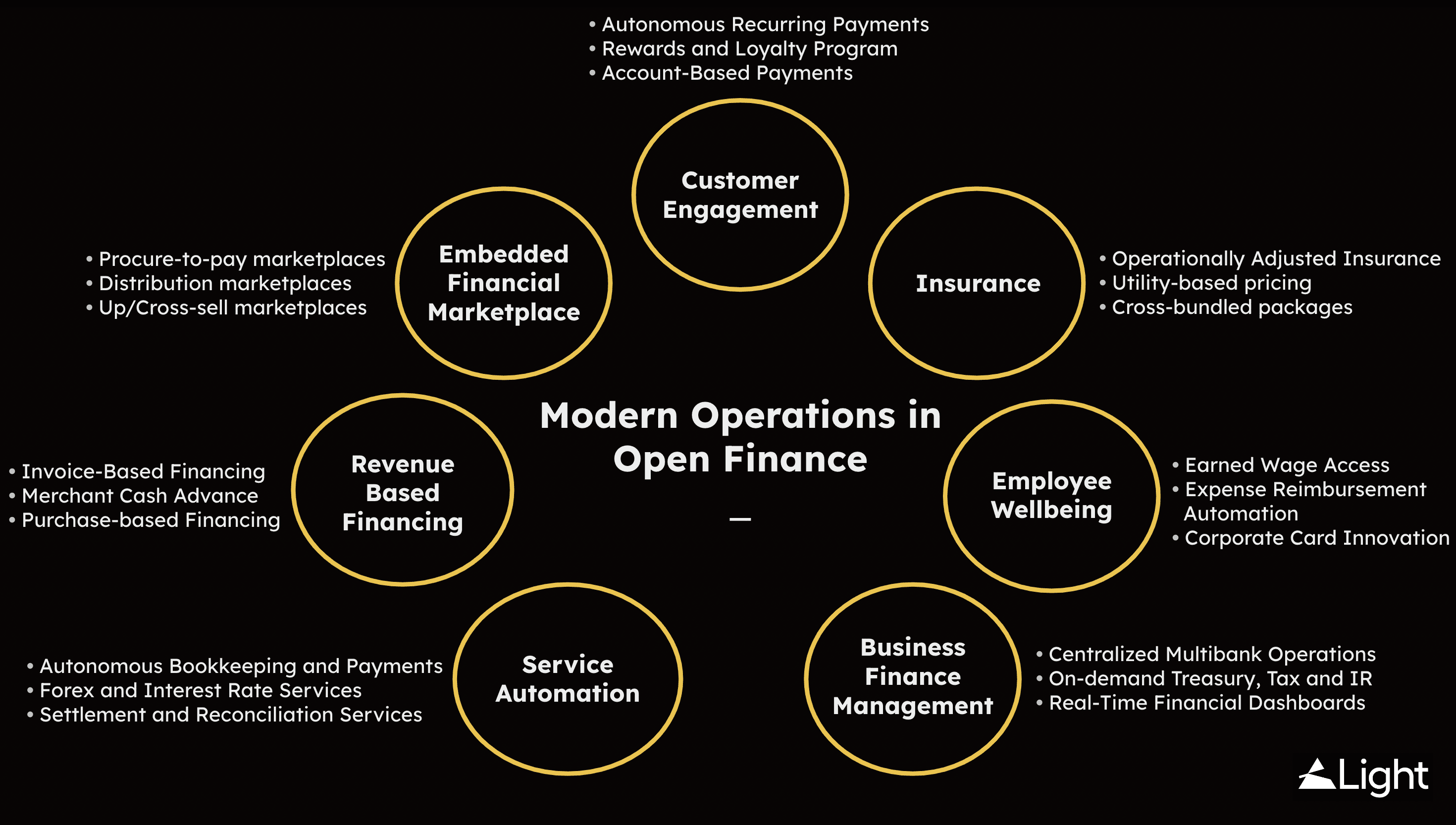

More practically, it has paved the way for a new era of financial services and products like centralised multi-bank operations in business finance, revenue-based financing, service automation, embedded finance marketplaces, streamlined corporate financial management through automation, and various flexible portability solutions.

Underlying all this financial activity is the crucial but often unseen role of APIs and TTPs, which facilitate fast and secure transfer of financial data between different points. Now… what if we go beyond automation and into autonomous financial operation? See this article for more.

In total, by allowing third-party access to financial data, open finance will enable several customer propositions for multinational businesses and their complex operations in a few different ways.

Figure 3: Created by Light

The Impact of "Open" on the Finance Function

Now, there's a lot happening for a finance leader, so let's try and nail a few things down that's gonna be key to keep an eye on.

1 — Streamlined Automation in Financial Operations

By automating traditional financial tasks, such as generating invoices, doing tedious reconciliation processes, monitoring payments and invoices, organising pay slips, and forecasting cash flow — all in a multinational operation workflow — will shift to being more strategic. Additionally, advanced providers can enable you to initiate cross-border payments and invoice requests directly from your accounting software, which is faster and more accurate than manually sending invoices.

It'll be a finance factory; transactions will be touchless as automation and blockchain reach deeper into finance operations. Now perhaps integrate this with a modern tool stack of Slack too and then we really start to talk.

2 — Improved Forecasting and Cash Flow in Business Finance Management

By aggregating all your accounts from multiple banks into one view, you will gain a comprehensive overview of your finances. With a clear understanding of your incoming and outgoing funds, you will have greater control over your cash flow. Additionally, improved data forecasting will provide you with accurate information, allowing you to effectively plan and manage your finances.

This also opens up revenue-based financing for you as a finance leader. Further, increased access to credit for businesses with limited financial history will be expanded. As open financial data provides businesses with real-time access to financial information, enabling them to effectively manage their finances through forecasting, credit applications, and faster payments.

3 — Getting Closer to Customers and their Financial Operations

Open finance allows third-party providers to access financial data held by banks, with the customer's permission. This means that businesses can send out a secure link to initiate a payment — rather than sending an invoice. Yes — scratch that invoice.

The link comes pre-populated with invoice details, eliminating the need for manual data entry. The funds are then sent directly from the buyer's account to the seller's in near real time. This process offers an alternative to traditional card or Direct Debit payments and ensures that businesses receive payments more quickly without the same transaction fees. By making it easier and quicker to receive payments, open banking can help finance leaders manage their cash flow more effectively and reduce the stress of waiting for payments to arrive.

4 — Data Analytics-Driven Financial Management Tools to Aid

By leveraging decentralized technology and smart contracts, open finance can streamline financial processes and reduce costs associated with intermediaries and manual processes. The role of finance then; with operations automated, finance will double down on business insights and service.

But… few organizations are putting in the effort to align and integrate their data, which prevents them from fully realizing the benefits of digital transformation. Those looking for a quick fix for their data issues will be disappointed as automation and cognitive technology can only make the process easier, not eliminate the hard work involved. This includes addressing issues such as commas, abbreviations, data-entry fields, nomenclature, and hundreds of similar factors that may seem trivial, but are crucial.

Data issues often go unnoticed by CFOs or other finance leaders, partly due to the technical nature of the problems, and partly because there is a lack of motivation for employees to bring them to the attention of top management. No one wants to be the one to deliver unpleasant news.

5 — Decreased Human Friction - Let My People Self-Serve

Most people don't require assistance with basic finance tasks and would prefer to receive answers from a digital voice instantly. Functions like budget inquiries, report generation, and more will be automated. Over time, intelligent agents will learn the specific business information a user needs and provide it proactively.

This shift will result in the replacement of data in spreadsheets with visually appealing and user-friendly information. Given the rising expectations for finance to be responsive and high-quality, it's crucial to get self-service right. If customers are left to handle things on their own, finance can't afford for them to become frustrated or dissatisfied.

In the End - There Is No Closing

With the capability to generate real-time actuals and forecasts, the traditional reporting cycles become less significant. The conventional distinction between operational and analytical data will start to fade away. Finance organizations will still have to fulfill the requirement for cyclical information from external sources, but there may also be a demand for more frequent performance updates from investors. The top organisations will adopt a new mindset: we don't close the books.

ERP providers are already incorporating technologies such as automation, blockchain, and cognitive tools into their offerings, but this won't eliminate competition. Expect changes in the ERP landscape as new entrants introduce specialized applications and microservices that complement and integrate with ERP platforms.

Also… why do we still call it ERP? This is finance.